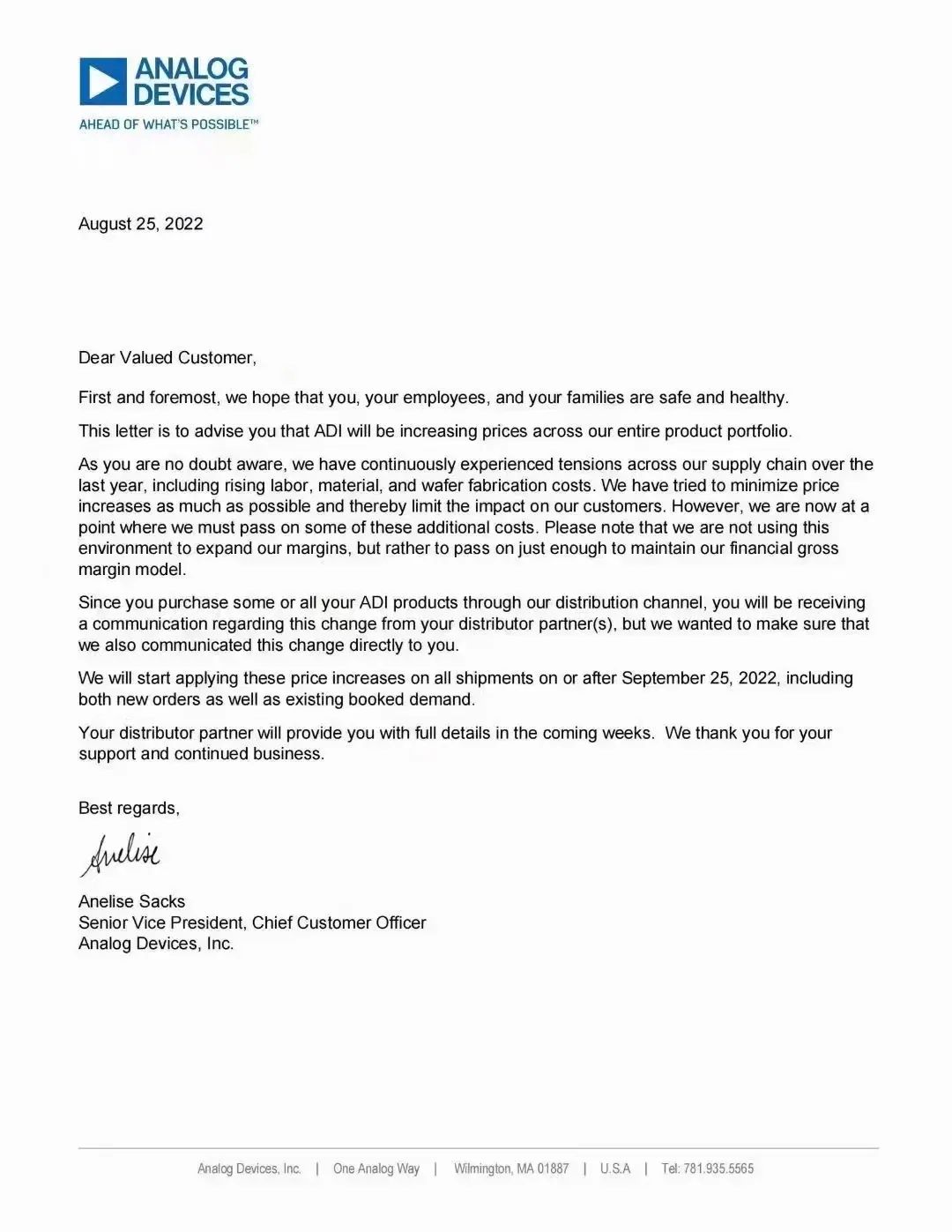

During this period of time, the analog giant ADI sent a letter to raise prices to occupy the headlines in the IC industry. Coupled with the price increases of foundries such as Samsung and GlobalFoundries, as well as the previous price increases of Intel, Broadcom and other factories, a new round of IC price increases has been start up. However, from time to time, during the peak period of the shortage of cores, the price increases of original factories and foundries are all for orders that are in short supply. Today, the weakening of demand has led to the cooling of the chip market. In addition, inflation has led to increased operating and expansion costs. To pass on unbearable costs.

At this stage, the market has shifted from lack of cores to excess. Except for some car-specific materials, there are not many materials that can maintain high prices, and ADI’s situation is no exception. The demand for consumer electronics has decreased, and it is difficult for terminal manufacturers to accept high-priced materials. Therefore, this round of price increases by ADI is difficult to stimulate the market.

After the previous acquisition of Maxim, ADI’s technical strength in the automotive and other fields has been improved. In the first three quarters of this fiscal year, the revenue of ADI’s automotive business more than doubled year-on-year. In the current downturn in consumer electronics, the help given to ADI by the automotive business is obvious.

However, ADI also admitted that economic uncertainty began to affect product bookings, and the company’s order volume decreased at the end of the second quarter, and the number of canceled orders increased slightly. It can be speculated that it is based on the conservative outlook that ADI issued this round of price increases to maintain its profit level.

The foundry insists on increasing prices, and the downstream competes with it

The price increase of wafer foundries runs through the entire process of this round of core shortages. At first, TSMC, UMC and other factories increased prices by double digits quarter by quarter. Now the demand for chips has been greatly reduced, and foundries have not stopped raising prices.

Recently, news broke that TSMC intends to maintain its plan to increase prices by 6%-8% next year. Samsung, the second largest foundry in terms of share, also intends to increase the price of wafers by 15%-20%, but this should be a price increase set for advanced processes, otherwise it is impossible to increase so high. GF, which focuses on mature processes, has recently reported that it will increase the price of some processes by 8% in 2023. In the face of the downturn in consumer electronics, the foundry price has increased rather than decreased, obviously to pass on the cost to the end.

Due to different process levels, various foundries have different specific reasons for considering price increases. But in general, the cost of operation and expansion has increased due to inflation, and the delivery time of equipment has also been extended due to lack of cores. However, under the decline in demand, many IC design factories have already begun to negotiate prices with wafer foundries due to high inventory, and even cancel long-term contracts at the risk of defaulting. During the period of sluggish demand, the games in the industry chain are all about risk aversion and self-preservation.

Previously, it was reported in the industry that the foundry price of mature processes fell by 10%, mainly due to the severe decline in the demand for panel driver chips (DDI), resulting in a decline in the capacity occupancy rate of related foundries. The demand for general-purpose chips has declined, and foundries have looked for opportunities from automotive demand. After some consumer customers withdraw their orders, the production capacity of TSMC and UMC has been quickly filled by automotive customers such as Infineon and NXP. It can be seen that there is still room for wafer foundries to flicker and move during the downturn in the market, at least until the supply of car cores is restored, there is still no need to worry about the production rate.

Consumer chip factory prices “not soft”

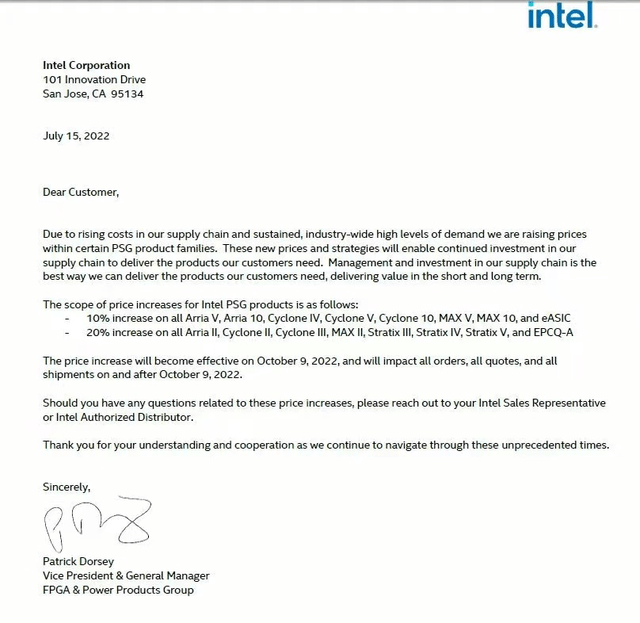

Previously, Intel reported that it would increase the prices of various PC processors by 10%-20%, server processors by 2%-10%, and workstation processors by 10% in October. Not only that, but FPGAs are also within the range of Intel’s price adjustment. According to the price increase letter from the industry, Intel will increase the price of FPGA product lines such as Arria, MAX, Stratix, Cyclone, among which the price of newer part numbers will increase by 10%, and the price of older part numbers will increase by 20%. From the 9th, all products shipped on and after that date will be billed at the new price.

In the second quarter, Intel’s revenue fell by more than 20% year-on-year, and it turned from profit to loss. This is probably the biggest reason for the price increase against the trend. However, from the perspective of demand, PC shipments have continued to decline in the past six months, and the pressure from brands and OEMs has also continued to increase. At this time, the increase in processor prices is tantamount to worsening the situation.

Under the sluggish demand, Qualcomm is also “unrelenting”. It was previously reported that Qualcomm will increase the price of new contracts by 4%, and will also increase the price of orders delivered from January 2023 by nearly 10%, which is obviously also It will increase the cost pressure of mobile phone manufacturers.

Since the beginning of the year, mobile phone and PC manufacturers have launched multiple rounds of order cutting to cope with the sudden drop in demand. Today, upstream chip manufacturers will still pass on the cost to the end, which may further weaken the willingness of downstream suppliers to stock up. From the current point of view, the traditional peak season of consumer electronics is going to fail this year. Even if chip factories increase prices against the trend, the effect of restoring gross profit margins may be very limited.

Conclusion: This round of price increases is different from the core shortage period

When the shortage of cores is in full swing, the price increase of original factories and foundries is mainly to reflect the huge demand, and to check the false demand such as repeated orders and excessive orders. Today, consumer electronics are sluggish, the demand for general materials has plummeted, and inflation and other environmental factors have led to a conservative trend in the industry chain, and they have been planning to “winter”.

Looking at the manufacturers of this round of price increases, ADI, TSMC, Intel and Qualcomm are all companies with high market shares in their respective fields. In other words, they have a strong voice and still have the ability to transfer costs downstream. For terminal manufacturers, they have to face the pressure of upstream cost and downstream demand at the same time, which may be difficult to withstand.